The qualified business income (QBI) deduction — also called the “Section 199a deduction” — is one of the many write-offs available to lower your tax bill and save money as a business owner.

When you file business taxes, you may be eligible to deduct a portion of your income to save money, but you’ll need to determine if you qualify for the QBI deduction first.

Let’s take a closer look at how the QBI deduction works and who qualifies, to determine if you can benefit from this tax write-off.

Qualified business income (QBI) is the net income or loss from a trade or business. This includes income generated from partnerships, S -corporations, sole proprietorships, and some trusts. QBI is used to determine the eligibility for the QBI deduction.

Generally, QBI includes the deductible portion of self-employed health insurance, self-employment tax, and contributions to qualified retirement plans such as SIMPLE and SEP plans.

There are several items that are specifically excluded from the calculation of QBI, including:

The IRS has a comprehensive list of items that aren’t included in the QBI calculation, so be sure to confirm what qualifies each year before you claim this deduction.

The QBI deduction was introduced as part of the Tax Cuts and Jobs Act (TCJA) in 2017. The TCJA changed tax rules affecting businesses, giving business owners new ways to save on federal taxes.

The QBI deduction has two main components: one based on the qualified business income (QBI) and another for the real estate investment trusts (REIT) and income from publicly traded partnerships (PTP).

While the QBI component of this deduction allows you to deduct up to 20% of your QBI from your business this compenent of the QBI deduction may be limited by the type of trade or business you own, the amount of W-2 wages paid, and the unadjusted basis immediately after acquisition (UBIA) of property held by your trade or business.

The REIT/PTP component of the deduction is 20% of the qualified REIT dividends and PTP income. Unlike the QBI component, the REIT/PTP component isn’t affected by W-2 wages or the UBIA of business property. However, there may be limits to the REIT/PTP component depending on the type of trade or business and your taxable income.

In total, the deduction is limited to the lesser of:

The TCJA only applies to tax years beginning after December 31, 2017, and expires for tax years end on or before December 31, 2025. Therefore, the time period to be able to claim this deduction and save on small business taxes is limited.

Keep in mind that there are other tax deductions you can qualify for after the expiration of the QBI deduction. As a business owner, it’s important to keep detailed records so you can work with a tax expert to maximize your tax savings at the end of each year.

Businesses have to meet certain criteria to qualify for the QBI deduction, so not every business is eligible. In this next section, we’ll outline who qualifies for the QBI deduction so you can determine if you qualify.

Only certain types of businesses are eligible for the QBI deduction. As mentioned above, the QBI deduction is available to sole proprietorships, partnerships, S corporations, trusts, and estates. All of these entities are considered pass through entities. C-corporations are not eligible for the QBI deduction since they are their own taxable entity.

You’re also not eligible for the QBI deduction if you earn income as an employee rather than as a business owner or partner.

Specified service trades or businesses (SSTBs) are only eligible for the QBI deduction if your income doesn’t exceed a certain threshold. You may also be within the phase-in range, which means you could still be eligible for the QBI deduction.

SSTBs are businesses that perform services in the fields of:

Your business or trade may also be considered an SSTB if you trade or deal in certain assets or if the primary asset of your business is the reputation or skill of one or more employees. For example, if your business income is a result of endorsing products or services or using your image, likeness, or voice, you’re considered an SSTB, and your income isn’t eligible for the QBI deduction if it exceeds the threshold.

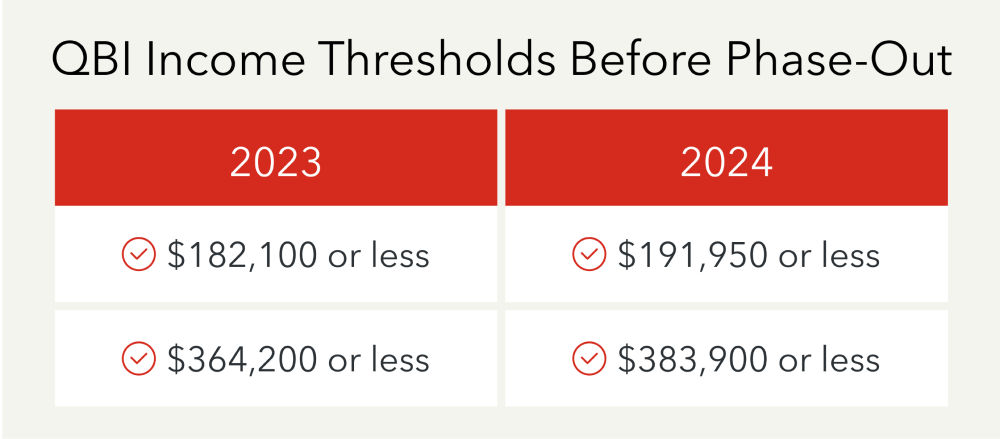

There are also income limits that may affect your eligibility or the amount you receive as a result of the QBI deduction. The 2023 income threshold is $182,100 for single filers and $364,200 for joint filers.

The income limits for the QBI deduction have increased slightly for 2024. Single filers must make $191,950 or less, and joint filers must make $383,900 or less. If you’re at or below these thresholds, you may be eligible for the QBI deduction.

At a certain income level, the QBI deduction begins to phase out (reduce in amount). For 2023, the QBI deduction phases out from $182,101 to $232,100 for single filers and $364,201 to $464,200 for joint filers.

The phase out income level changes with each tax year. In 2024, the QBI deduction will be phased out if your income is between $191,951 to $241,950 for single filers and $383,901 to $483,900 for joint filers.

Once you reach the upper threshold of the phase-out income limit, you’re no longer eligible for the QBI deduction. If your income is within the phase-out range, you may be eligible for a smaller QBI deduction.

Generally speaking, the QBI applies to income that’s connected to a sole proprietorship, partnership, S corporation, or a certain type of trusts. This includes the deductible portion of self-employment tax and contributions to qualified retirement plans.

While various types of business income are eligible for the QBI deduction, certain types aren’t. Wage income, income that’s not included in taxable income, capital gains and losses, and certain other types of income are excluded. The QBI deduction also excludes income generated by foreign currency gains, commodities transactions, and certain dividends.

In order to be eligible for the QBI deduction, you also need to conduct business within the United States. Income that’s not connected to business conducted within the United States isn’t eligible for the QBI deduction.

If you have any questions about the types of income that qualify for the QBI deduction or whether your business qualifies, consult a tax expert who can evaluate your situation.

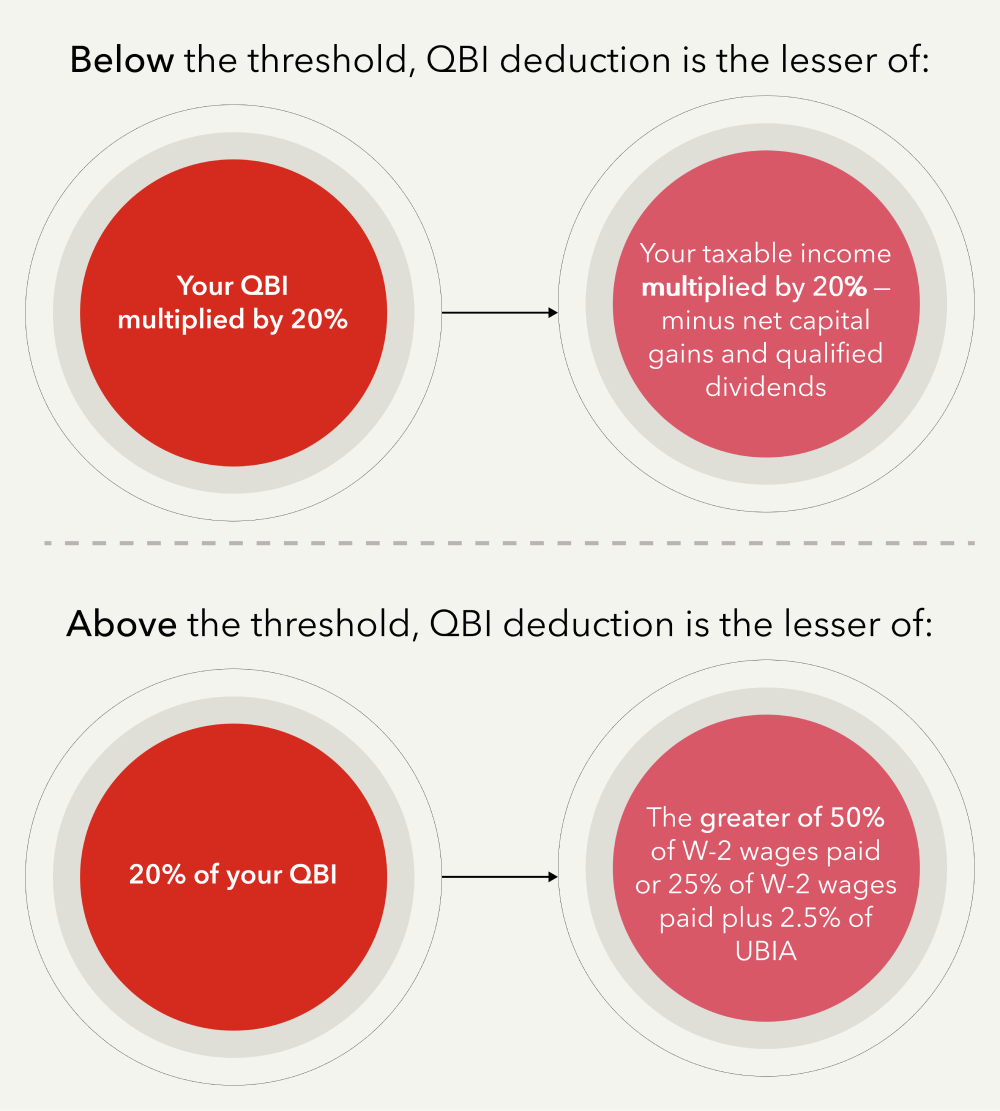

If you want to calculate your QBI deduction, you need to determine whether you’re below or above the income threshold for the QBI deduction phase-out.

If you’re below the threshold — even if you’re an SSTB — your QBI deduction will be the lesser of:

In total, your QBI can’t be more than 20% of your taxable income.

For businesses that are above the income threshold, your QBI deduction will be the lesser of:

When your income exceeds a certain threshold as an SSTB, you may no longer be eligible for the QBI deduction. Eligibility for the QBI deduction may also depend on the type of income your business generates.

Keeping detailed records is an essential part of maximizing your tax deductions and reducing your tax bill. You can also get help from a tax expert to make sure you’re taking advantage of all the deductions and tax credits you’re eligible for.

No matter what moves you made last year, TurboTax will make them count on your taxes. Whether you want to do your taxes yourself or have a TurboTax expert file for you, we’ll make sure you get every dollar you deserve and your biggest possible refund – guaranteed.